Inflation, Jobs, and the Economy are shaping everyday decisions for households across the country. For many families, the inflation impact on personal finances is felt at the grocery store and at the gas pump. Rising prices affect the cost of living and wages, even when nominal pay checks look unchanged. Understanding employment trends and inflation helps you plan, while budgeting during inflation keeps you on track when every dollar matters. This brief guide offers clear steps to stay financially resilient as prices move and the job market shifts.

In more general terms, today’s topic can be described through price pressures, wage dynamics, and the health of the labor market. Economic conditions and monetary policy shape how households plan, spend, and save. Think of it as macro trends influencing daily budgets, shopping choices, and long-term goals. By framing inflation and employment as interconnected forces, you can build resilient strategies that align with evolving market realities.

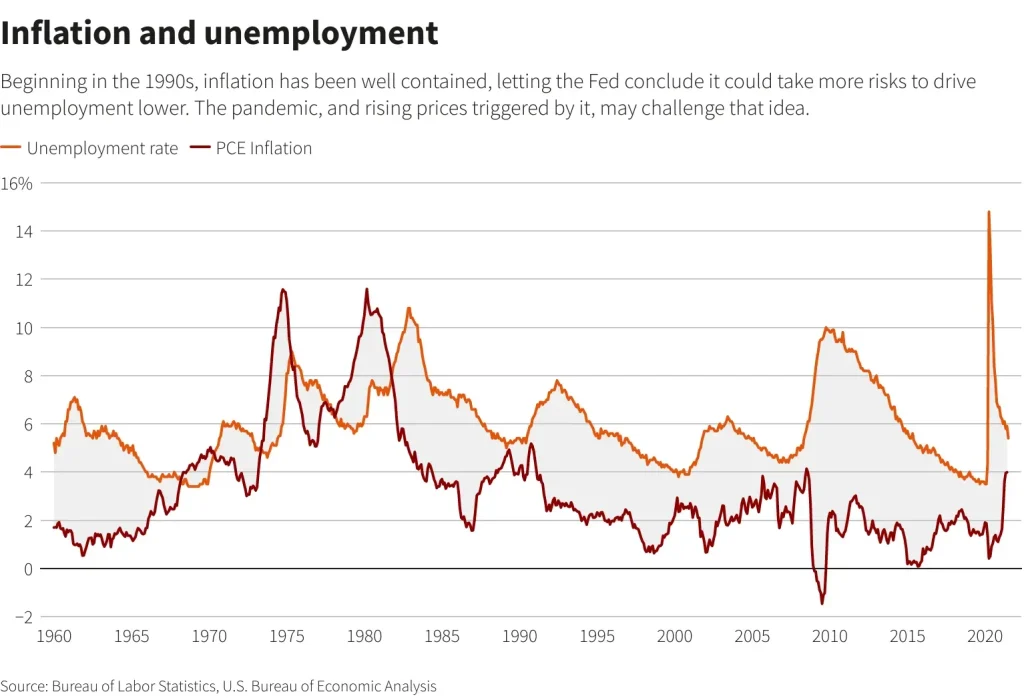

Inflation, Jobs, and the Economy: What It Means for Your Wallet

Inflation, Jobs, and the Economy shape everyday money decisions more than you might think. When prices rise for food, energy, housing, and transportation, your grocery bill and utility payments can take a bigger bite out of every paycheck. Understanding the inflation impact on personal finances helps you anticipate these changes, adjust your plan, and protect what you save for future goals. Even if your nominal salary remains the same, real purchasing power can shrink if wages don’t keep pace with price gains, so these forces feel personal—it’s about the dollars you can buy with today’s money.

Worker responses to rising prices also play a role. When jobs are plentiful, workers may push for higher pay or switch to roles with stronger wage growth, sustaining higher consumer demand. In a looser job market, the opposite can happen, and households tighten belts to cover fixed expenses. These employment trends and inflation dynamics shape your budget, debt decisions, and long-term plans.

Practical Budgeting During Inflation: Strategies to Protect Your Wallet

Smart budgeting during inflation starts with separating essentials from non-essentials and building in flexibility. A robust emergency fund—three to six months of essential expenses—reduces the impulse to take on high-interest debt when prices spike. By automating savings and reviewing how the cost of living and wages align with your income, you can buffer the impact of price shocks and keep momentum toward your goals. This approach directly addresses budgeting during inflation by keeping essential spending covered while giving you room to adapt.

Beyond the emergency cushion, manage debt and diversify income. Prioritize high-interest debt repayment and consider refinancing large loans when appropriate to lower carrying costs. In the longer run, inflation-protected assets and regular investing can help preserve purchasing power, tying into the idea of economic changes and your wallet. Tracking expenses and staying mindful of cost of living and wages can keep you on course when the economy shifts.

Frequently Asked Questions

How do Inflation, Jobs, and the Economy shape the inflation impact on personal finances and the cost of living and wages?

Understanding the inflation impact on personal finances helps you see how rising prices affect daily life. When prices climb faster than wages, the cost of living and wages balance shifts, reducing purchasing power even if your nominal pay stays the same. Employment trends and inflation influence how quickly wages respond to price changes, so monitor both income and expenses. To protect your wallet, build an emergency fund (three to six months of essential expenses), automate savings, and prioritize essential spending. Regularly review debt costs and target high-interest balances, while considering inflation-hedged options for longer horizons.

Which budgeting during inflation practices align with current employment trends and inflation to shield your wallet amid economic changes?

Budgeting during inflation means separating essentials from non-essentials and adjusting as employment trends and inflation shift. Focus on core needs—housing, utilities, groceries, healthcare—and seek value without sacrificing quality. Create a flexible budget, automate savings, and explore ways to reduce debt costs, including refinancing or prioritizing high-interest payments. Diversify income when possible and consider inflation-protected assets to preserve purchasing power. Stay prepared for economic changes and your wallet by regularly reviewing spending, goals, and investments.

| Theme | Key Points | Practical Takeaways |

|---|---|---|

| Inflation and Purchasing Power | Prices rise; money buys less; real purchasing power can shrink if wages don 0t keep pace. |

Monitor price trends; plan purchases; consider inflation-resilient saving and investments. |

| Job Market and Wages | Strong jobs growth can raise wages; softening jobs may reduce wage growth and increase budgeting caution. | Track employment trends; negotiate raises; upskill to improve earning potential. |

| Impact on Spending | Higher prices raise cost of essentials; discretionary spending can shrink; saving becomes harder. | Prioritize essentials; automate savings; review bills and consumption. |

| Budgeting Response | Budget should adapt to price and labor conditions; flexible plans help absorb shocks. | Separate essentials from non-essentials; build a buffer for price spikes. |

| Emergency Fund | Three to six months of essential expenses buffers shocks and reduces debt temptation. | Set a monthly target; automate contributions; grow the fund gradually. |

| Debt Management | Higher interest rates increase debt costs; inflation and slowdowns can affect repayment power. | Prioritize high-interest debt; consider refinancing; plan to reduce interest costs. |

| Purchasing Power Protection | Inflation can erode long-term purchasing power if not matched by income; inflation-linked assets help. | Diversify income; invest in inflation-protected assets; maintain regular investing and saving. |

| Smart Shopping and Bills | Prices, coupons, and negotiating recurring bills can materially affect monthly cash flow. | Compare prices; negotiate terms; cut unnecessary recurring costs. |

| Long-Term Planning | Dynamic job market and inflation require continuous skills development and diversified income. | Invest in training; diversify income; maintain conservative savings in uncertain times. |

| Personal Scenarios & Action Plan | Real-world scenarios illustrate adaptation needs; tracking expenses and adjusting plans helps stay on track. | Track expenses; anchor a budget to essentials; build skills; review investments and debt strategy. |

Summary

Conclusion